The Everything Bubble

The Crash that Nobody Can Stop

The global economy is hurtling towards the biggest market crash of the last century. It will ruin countless lives for years if not decades, upend the geopolitical order, and pour gasoline on every domestic political fire. This economic crisis was always going to happen, regardless of who the leaders of the G20 were at the time. The starting gun might be unique, as is the skill or ineptitude of political figures, but the crisis itself was baked in from the start of the post-WWII Baby Boom.

The Irrational Economy

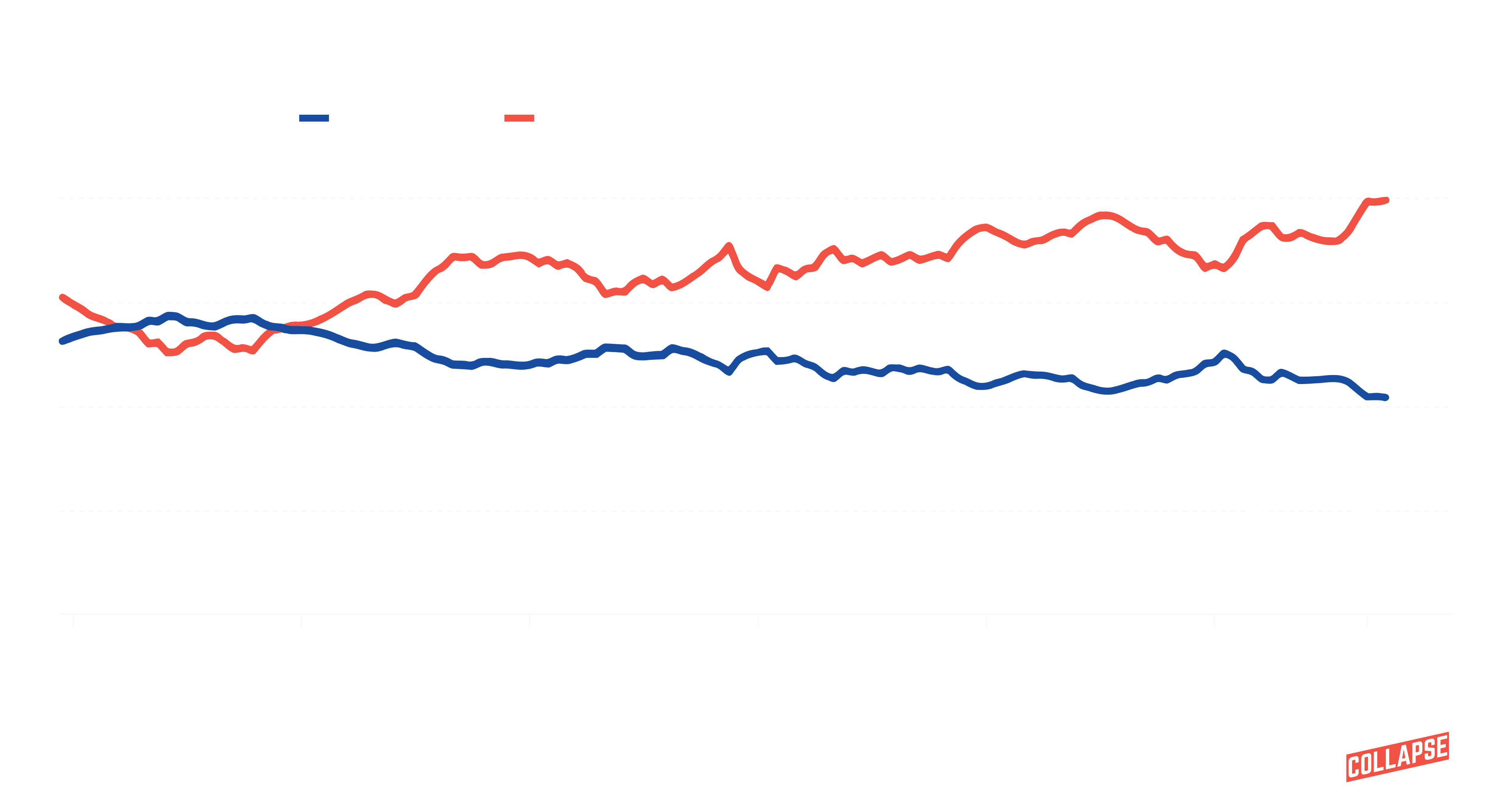

The last year has been one of the most chaotic in living memory for economists as the US government has announced, cancelled, implemented, threatened, re-cancelled and/or re-implemented a dizzying number of tariffs. Meanwhile the federal government gutted spending to entitlements, fired tens of thousands of workers, shutdown the government multiple times, and implemented an immigration policy that expelled 1.2 million people from the labor pool. And yet, the US economy did not crash, no supply shock came, in fact the economy continued to grow. While recent data points to lethargic growth, that’s a lot better than what a lot of people were predicting, me included. So what’s going on?

The United States has become a K-shaped economy, where more than half of consumer spending is done by the wealthiest 10% of the population. This is partly just the typical sale of expensive goods and services to the wealthy, partly the result of the AI Bubble. Spending on AI projects, investment in AI startups, and all the related supply chain expenditures are helping to prop up an otherwise lethargic economy, and drive the stock market to new heights.

However, AI spending does not explain the why we haven’t seen major tariff induced supply shocks. That answer lies with the scale to which companies overstocked prior to the start of Trump’s second term, and then proceeded to sell off that inventory over the course of 2025, at one point yielding a net decrease in overall investment in Census data. This means that selloff nearly equaled all investment in AI.

While market watchers, and even investors, are waking up to the reality that the AI Boom is really a Bubble, for most the expectation is an eventual market correction contained wholly to AI stocks. That is the same expectation investors have had in the face of every bubble, and it has never played out that way. I’m on record about how Big Tech as a whole is unlikely to survive the popping of the AI bubble, but what hasn’t been well examined is how this will get back to the rest of the economy. And to best understand that, we have to look at a housing bubble nobody’s talking about.

Generational Wealth

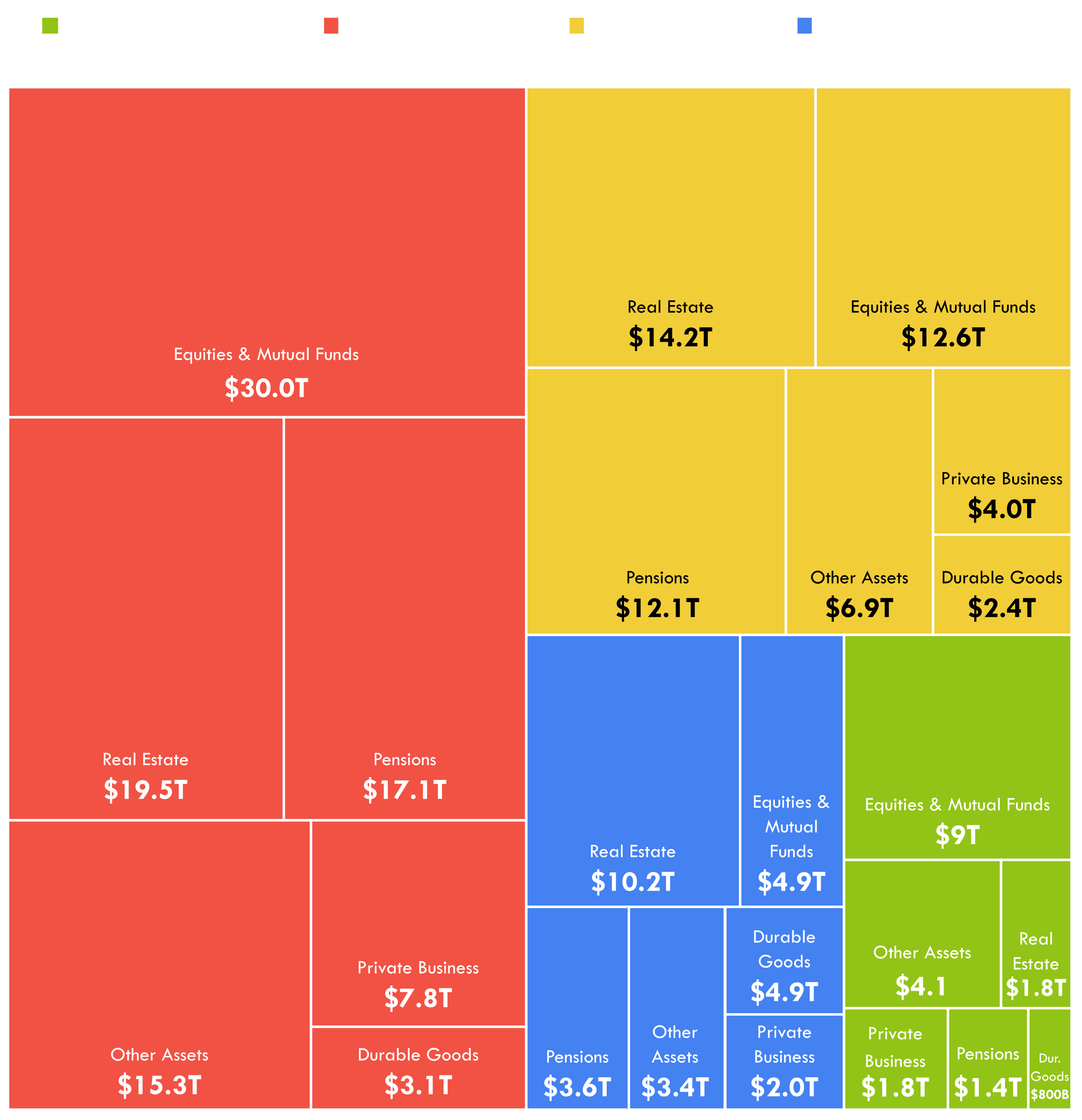

2025 marked Peak Retirement in the Untied States, with 4.2 million people turning 65. According to the Social Security Administration, approximately 58 million people in the US were over 65 as of January 2026. That’s the overwhelming majority of Baby Boomers and the Silent Generation who collectively control around 59% of assets in the Untied states. The bulk of that wealth is tied up in Real Estate, Pensions, Equities & Mutual Funds. These are asset classes generally seen as extremely resilient.

Every market is predicated on there being more buyers than sellers. That’s what makes home ownership so attractive for people planning for retirement, the assumption that demand will always outstrip supply because people always need homes. But now retirees have so much more wealth than working age people that when they try to sell off assets, say during a market crisis, they’ll be selling to a market that won’t be able to buy.

A crash in real-estate prices would be bad enough, but pension funds are a time bomb that could wipe out generations of wealth, thanks to a recent trend called the Alternatives Surge. 25 years ago pensions assets were allocated almost entirely to Fixed Income Investments (bonds, Treasuries, and CDs) that offered low risk, reliable payouts to retirees. In recent years “Alternatives” like stocks, private equity, real-estate, and hedge funds have come to take up around 34% of all pension fund asset classes. Worse, while fixed income investments used to rely on Treasury bonds, they now lean more toward high-yield bonds, commercial real estate loans, student loans and credit card debt. So far more retiree wealth is at risk during the next crash than what is reported.

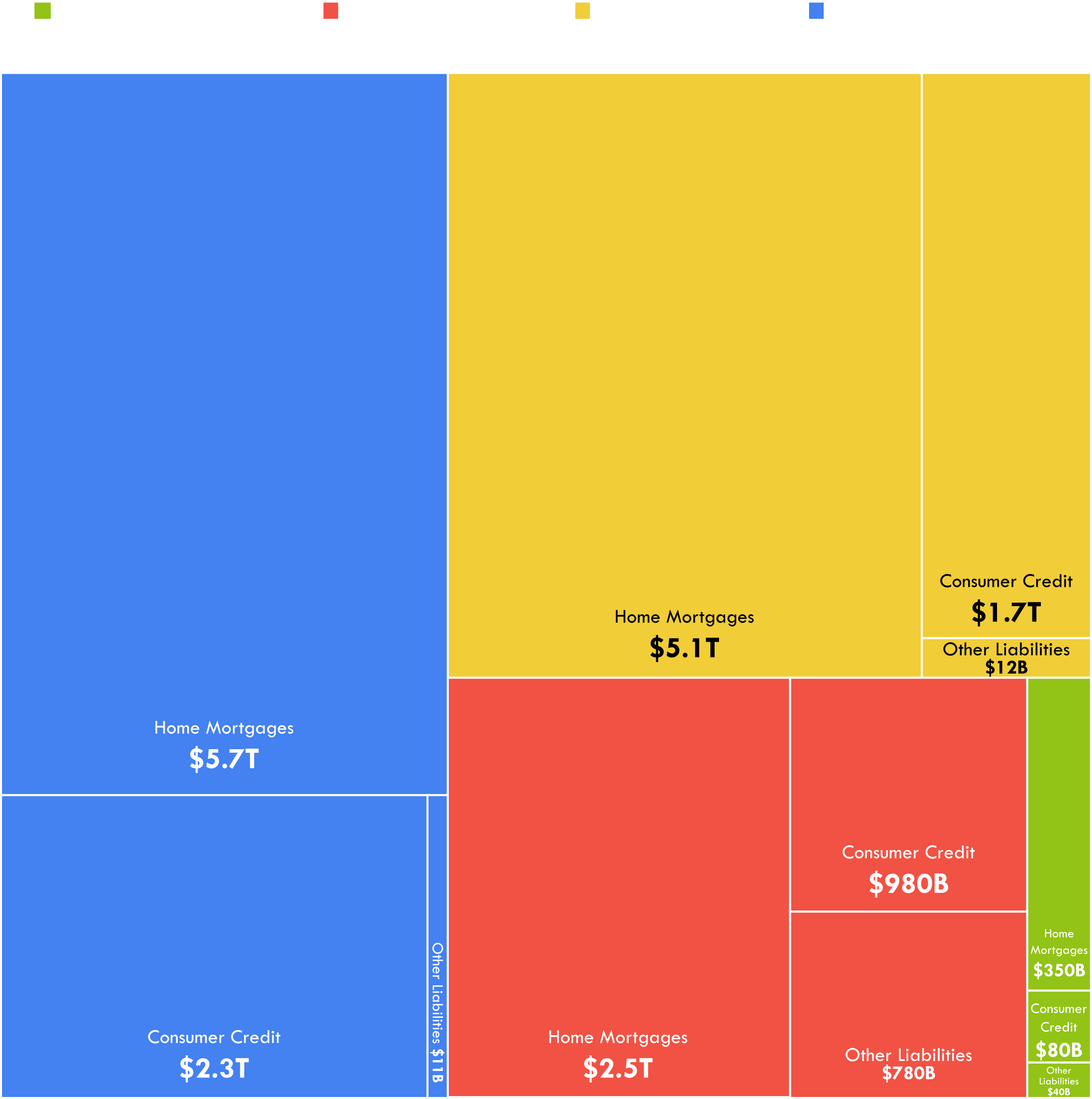

So, the generations with most of the wealth are absolutely dependent on the idea that the younger generations will be solvent forever, and get rich enough to buy what they will eventually need to sell. While Millennials and Gen Z are finally starting to build wealth, its simply not big enough to keep the retirees afloat, and that’s before you factor in that younger generations have far more liabilities, over $8.1 Trillion as of Q3 2025. Ergo, Millennial and Zoomer wealth, assuming no depreciation in any of their assets, is closer to $18 Trillion than $26 Trillion, further reducing their ability to leverage their wealth to borrow money, and thereby plug the hole in the economy.

Crisis Point

We’re already seeing the beginnings of this crisis. Bankruptcies filing in 2025 rose by 11%, with business filings rising by 7.1% a 15 year high. This shouldn’t be much of a shock given that interest rates are still at some of the highest levels they’ve been since the Crash of 2008, and consumer spending for more mid and lower market products and services is down. Meanwhile, credit card debt has grown to over $1.28 Trillion, and auto loan delinquency rates are at a 14 year high. And on top of all of this, the United States and Israel just started a regional war in the Middle East, further threatening global oil flows. Its anybody’s guess what actually kicks this whole thing off, but its probably not a good idea to kick off an energy supply shock when the Tech Sector is already struggling to operate and build new data centers thanks to their insatiable demand for power.

Regardless of what specific event kicks off investor panic, the situation is is too precarious and too deep for a crash to be avoided. I know I’m a broken record, but we will reach a crisis point, one where the market panics, wealth is wiped out, and the current generation of leaders will be incapable of arresting. Most retirees will see their equity wiped out, leaving them with very little to live on. Bankruptcies will destroy the credit worthiness of millions, consumer spending will grind down to nothing, unemployment and homelessness will surge. The only solace ordinary people will be able to take is that many of the world’s wealthiest people are so overleveraged that they’ll be left penniless by this crash as well.

While I hate stating the obvious, the crisis will not be limited to the United States. A massive contraction in American investor capital and consumer spending on the scale what we can expect would send shockwaves across the world. The hardest hit would include major US trading partners like Mexico, Canada, China, and Germany, major energy exporters, and of course countries overly reliant on foreign capital. But nobody would escape this crisis, mainly because their own baby boomers would follow a similar pattern of behavior as their American counterparts during the panic.

This won’t be a recession with a speedy recovery either. Even if Trump were replaced tomorrow with a clone of FDR, under the best of circumstances it would likely take more than a decade just to return to some semblance of economic normalcy. The panic will upend governments everywhere, beloved or reviled no political leader will escape unscathed as people demand solutions that no one can immediately provide. Thermostatic backlash will produce some unusual changes to national governments and economic policy. In many cases what was once unthinkably radical will become pragmatic policy. But that’s a story for another day.